Credit scores play a significant role in many areas of our financial lives - not just in obtaining real estate mortgages, but also when applying for credit cards, auto loans, and sometimes with employers, utility companies, and insurance providers. Maintaining and improving your credit score is a cornerstone of financial health and responsibility. Here are some key points about credit scores and actionable tips to help you boost yours.

What is A Credit Score?

A credit score is a numerical representation of your ability to borrow money and repay it on time. It’s presented to consumers and third parties in the form of a credit report when requested. A high credit score represents responsible financial behavior, making you a more attractive applicant to lenders and often unlocking additional options and lower interest rates.

How to Know What My Credit Score Is?

Companies like Experian, Equifax, and TransUnion compile information to create and deliver credit reports. In addition to these three major credit bureaus, services like Credit Karma, along with many credit card accounts and banking institutions, offer access to credit information. While some companies charge to view and monitor your credit, others include this access as part of an existing subscription or service.

What is a Good Credit Score?

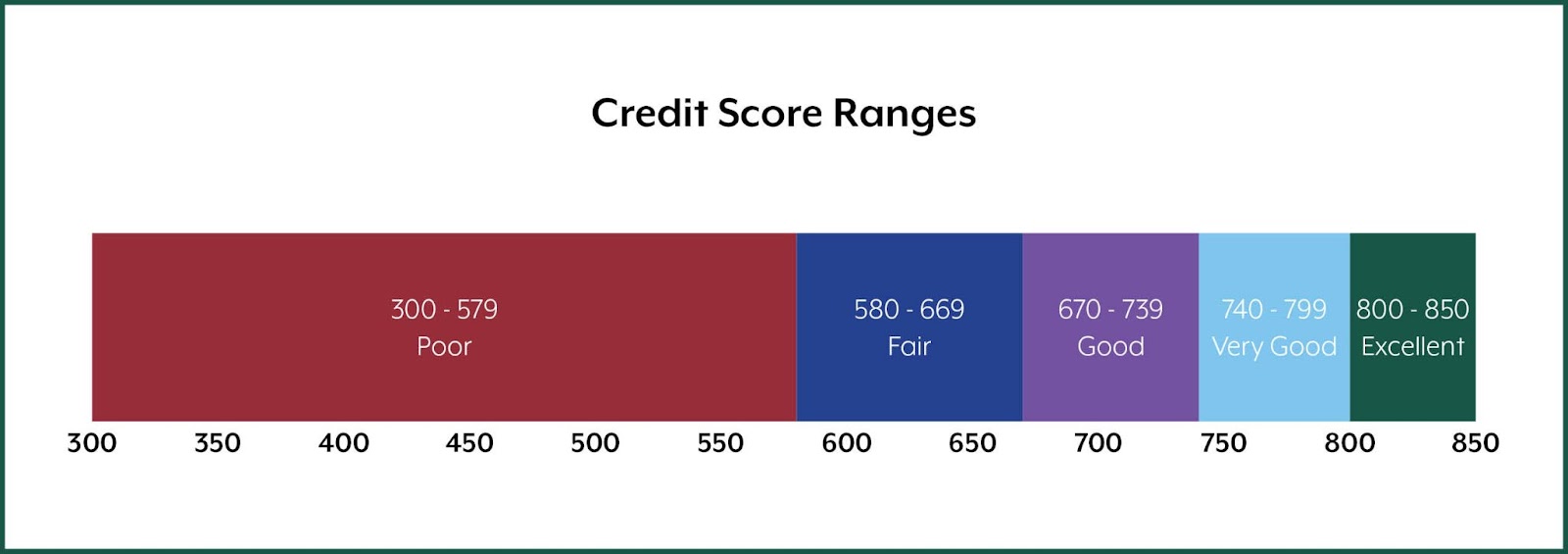

A good credit score typically falls in the mid to high 600s and above. Credit scores range from 300 to 850 and are typically broken down into five different categories.

Poor: <579

Fair: 580 - 669

Good: 670 - 739

Very Good: 740 - 799

Exceptional: 800 - 850

Keep in mind that your score may vary slightly depending on the scoring model used, such as FICO, VantageScore, or industry-specific model. Each evaluates different factors and weights to calculate your score.

What Affects and How Do I Improve My Credit Score?

Personal information such as your address, income, employment, and demographics does not directly impact your credit score. However, factors like income and employment can influence the amounts lenders are willing to loan. The factors that do impact your credit score also offer guidance on how to improve it. While it may feel like a bit of a catch-22, you need credit to build credit. Here are the basic principles that can help you grow your credit score effectively.

Payment History

This is typically the most important factor in determining your credit score. It reflects your track record with past loans and on-time payments. Overdue loans and past due bills signal risk to lenders, making it less likely they’ll extend you credit. The best way to improve this is pretty straightforward: pay your bills - especially those tied to your credit - on time and consistently!

Credit Usage

Let’s say you have a credit card with a limit of $10,000. If you put $10,000 worth of charges on it, that’s 100% credit utilization. It’s recommended to keep spending at or below 30% of your total credit available - in this case, $3,000. While it may seem misleading to have a limit you’re advised not to fully use, higher utilization (over 30%) can indicate to lenders that you’re at risk of overextending yourself or defaulting on the loan. Paying off your balance in full each month resets your utilization and demonstrates that you are using credit responsibly and within your means.

Credit History & New Credit

The age of your credit accounts, both individually and as an average across all accounts, plays a part in your credit score. Keeping credit lines open and healthy for extended periods signals reliability and stability, and boosts the confidence of future lenders. Although opening a new line of credit isn’t necessarily harmful, it can bring your average credit age down and may give the impression that you are overextended. It is best practice to not open many new credit lines in a short timeframe. Similarly, closing accounts can reduce your average credit age and may impact your score, as closed accounts remain on your report for seven to ten years.

Inquiries

Inquiries occur when a third party reviews your credit report as part of a loan or credit application. There are two types of inquiries:

Soft inquiries: These occur when you check your own credit report, when it’s checked for pre-approval, or for non-lending purposes. They do not affect your credit score.

Hard inquiries: These happen when a lender reviews your credit report to determine your eligibility for a loan or new account. While hard inquiries only impact your FICO score for 12 months, they remain on your report for two years.

Credit Mix

As mentioned earlier, credit comes in two different forms:

Installment credit: These are loans with fixed payments, such as car loans and mortgages.

Revolving credit: These cover accounts like credit cards, where the balance and payments vary.

Properly managing both types can increase your score and show your ability to handle diverse financial responsibilities.

What is a Good Credit Score to Buy a House?

While a “good” credit score is generally considered to be 620 or higher, most mortgage lenders use this as a benchmark, according to the National Association of REALTORSⓇ. However, this can vary. For example, FHA loans are geared more towards first time homebuyers and may accept scores as low as 500. When preparing to apply for a mortgage, it’s best practice to not open any new cards, focus on paying 100% of revolving debt, and keep usage under 30% for 12 months. Although it is possible to secure a mortgage with a lower credit score, having a higher score can result in better interest rates and payment terms.

While we are not financial experts, we do understand just how vital credit scores are in real estate as well as many other parts of life. If you have questions or need guidance, please don’t hesitate to contact us - we’d be happy to connect you with additional resources and provide support for your real estate needs.